| |

| Market Update |

| |

|

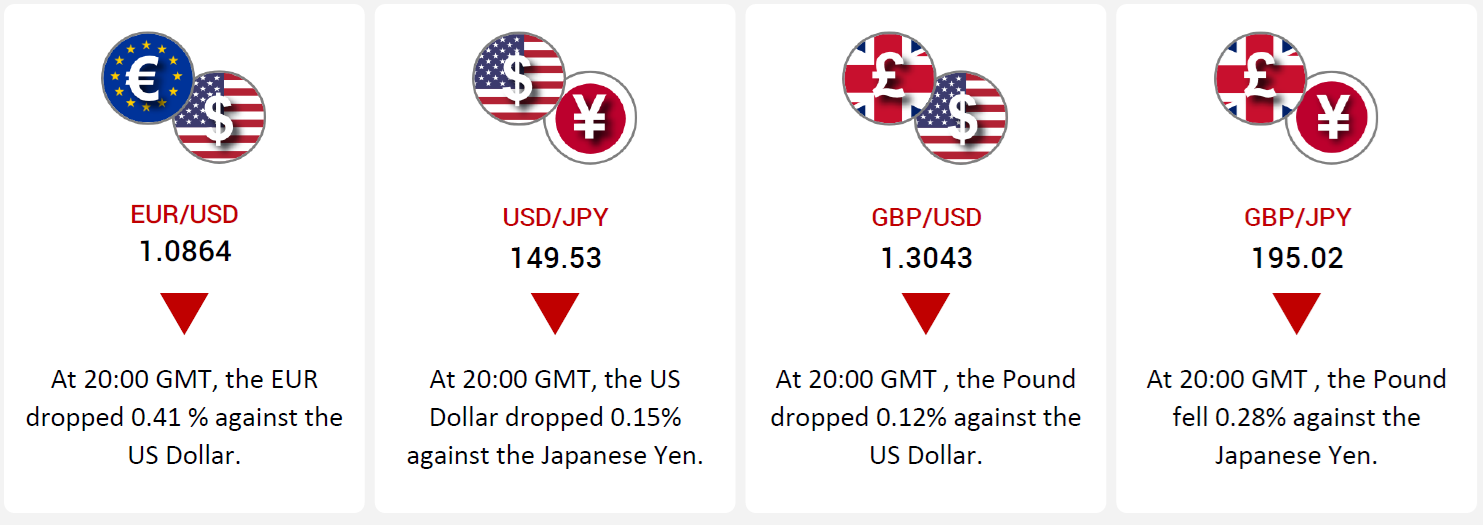

This week, major currency pairs displayed mixed performance driven by central bank actions and global economic indicators. The EUR/USD fell 0.41%, pressured by a stronger U.S. dollar and the European Central Bank's (ECB) decision to cut borrowing costs by 25 basis points. Weak inflation and GDP growth in the Eurozone raised expectations for further ECB rate cuts, weakening the euro.

Meanwhile, the USD/JPY fell by 0.15% despite solid U.S. economic data. Japan’s lower-than-expected inflation and sluggish GDP growth strengthened the yen, but ongoing U.S. rate hike expectations supported the dollar.

The GBP/USD fell 1.2%, as strong U.S. consumer spending bolstered the greenback, while a surprise rise in UK retail sales wasn’t enough to counter speculation of future Bank of England rate cuts. Similarly, GBP/JPY dropped 0.28% amid concerns over the UK's inflation outlook and Japan’s stagnating economy.

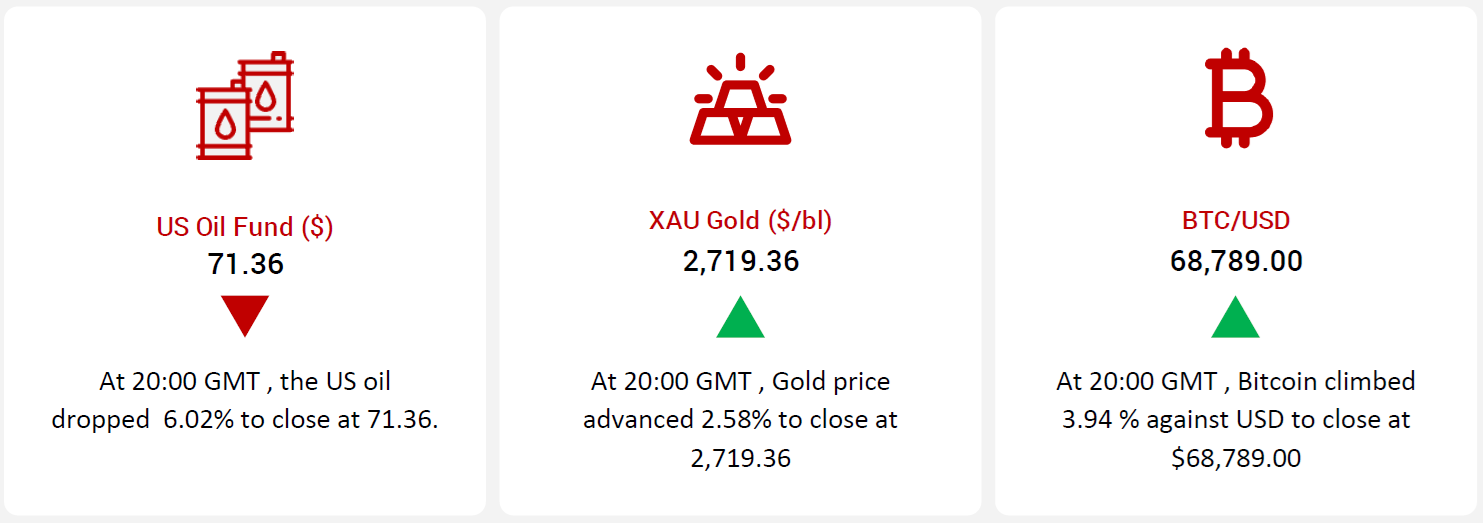

In commodities, oil prices dropped as fears of supply disruptions eased and weak demand signals from China contributed to a negative market outlook. Conversely, Bitcoin rose, boosted by optimism surrounding U.S. regulatory support post-election and interest rate cuts globally. Finally, gold prices advanced, benefiting from geopolitical tensions and declining U.S. Treasury yields.

|

| |

|

|

Key Global Commodities

|

|

| |

| |

| |

|

| |

|

|

EUR/USD

|

|

|

Euro under pressure as dollar strengthens

|

|

| |

|

|

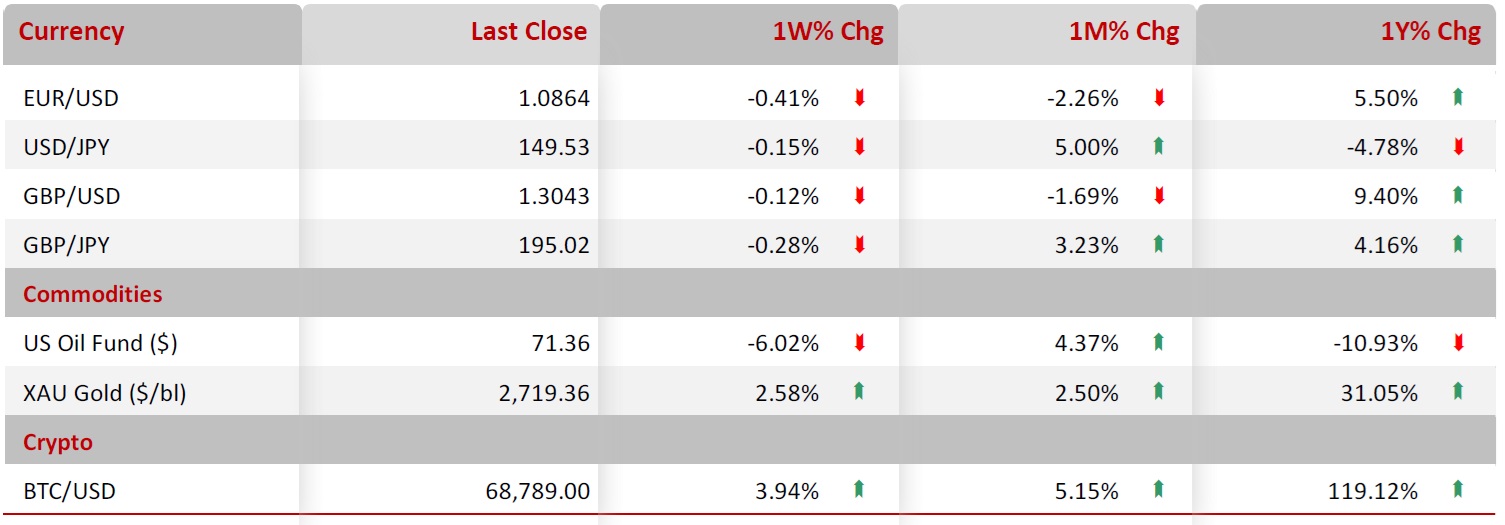

The EUR/USD decline 0.41% during the week as the US dollar maintained its strength and rate cuts by European Central Bank (ECB) raised hopes for further rate cuts.

The ECB lowered its borrowing costs by 25 basis points, leading to an increase in rate-cut expectations. While date this week showed that the annual inflation dropped in September. Overall, growth in 3Q24 GDP and drop in inflation, well below the ECB's 2% target suggests the likelihood of further rate cuts from the ECB, further weakening the euro. Consequently, ECB President Lagarde failed to give further guidance on the rate cut outlook.

The US dollar remains strong, supported by a solid labor market and the recent rate cuts from the Federal Reserve. The unemployment rate has stabilized at 4.0% and encouraging consumer spending data is enhancing confidence in the dollar's resilience. Moreover, increased bets for a Trump win have supported the greenback.

|

|

| |

| |

| |

|

|

USD/JPY

|

|

|

Yen gains ground against Dollar

|

|

| |

|

|

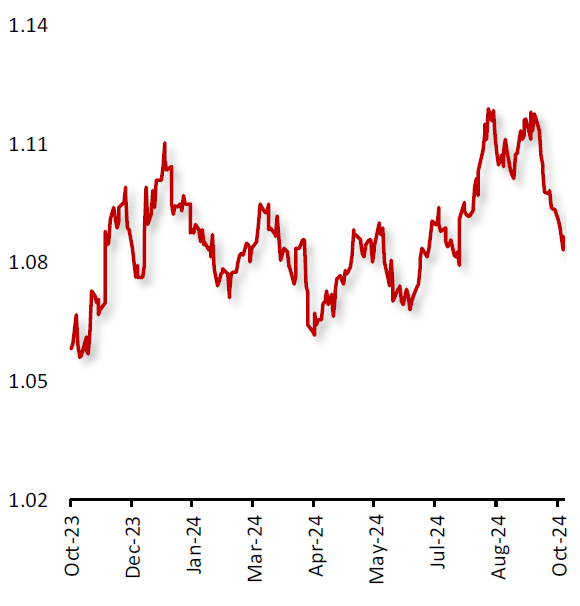

The USD declined 0.15% against JPY this week amid hawkish comments from Federal Reserve officials. Despite the rise in US Producer Price Index showing year-on-year increase to 2.8% following a solid nonfarm payroll report for September and a declining unemployment rate of 4.0%. The NY state manufacturing activity contracted modestly in October amid rise in treasury bonds yield.

In Japan, inflation dropped more than expected in September. The economy faces persistent challenges, with the Bank of Japan (BoJ) maintaining its ultra-loose monetary policy. Industrial production dropped August. Further, Japan's GDP growth stagnated at 0.2% for Q3 2024 amid inflation remaining low at 1.5%, far from the BoJ’s 2.0% target which is strengthening JPY.

|

|

| |

| |

| |

|

|

GBP/USD

|

|

|

Sterling struggles against dollar

|

|

| |

|

|

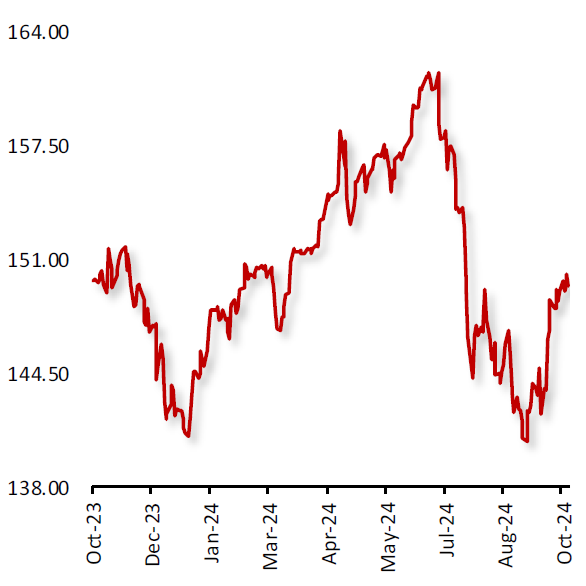

The GBP/USD fell by 1.2% this week amid continued strength in the US dollar. The economic data indicated resilience in consumer spending, fuelling speculation that the Bank of England would resume cutting interest rates next month. Moreover, UK retail sales unexpectedly rose in September.

In contrast, the US dollar remains buoyant, bolstered by a robust labor market and the Federal Reserve’s recent rate cuts. The unemployment rate in the US has held steady at 4.0%, and strong consumer spending figures are reinforcing confidence in the dollar’s strength. Moreover, investors await further cues from the US Fed for its interest rate policy.

|

|

| |

| |

| |

|

|

GBP/JPY

|

|

|

Pound faces challenges against Yen

|

|

| |

|

|

The GBP declines 0.28% against JPY this week driven by growing economic concerns in the UK. Japan's consumer price index inflation slightly exceeded expectations in September, with core CPI rising to 2.4% YoY, though headline inflation fell to 2.5%. Amid concerns about the Bank of Japan's ability to raise interest rates further, new Prime Minister Shigeru Ishiba indicated that the country is not ready for another hike. Industrial production declined in August, and Japan's GDP growth stagnated at 0.2% for Q3 2024.

In the UK retail sales grew by 0.3% in September 2024, driven by a 2.5% increase in non-food retail, despite a significant decline in supermarket sales. Overall, quarterly retail volumes rose by 1.9%, signaling cautious optimism as retailers prepare for the crucial holiday season. Additionally, Britain’s annual inflation rate dropped to a three-year low in September, raising speculation that the Bank of England may resume interest rate cuts next month.

|

|

| |

| |

| |

|

|

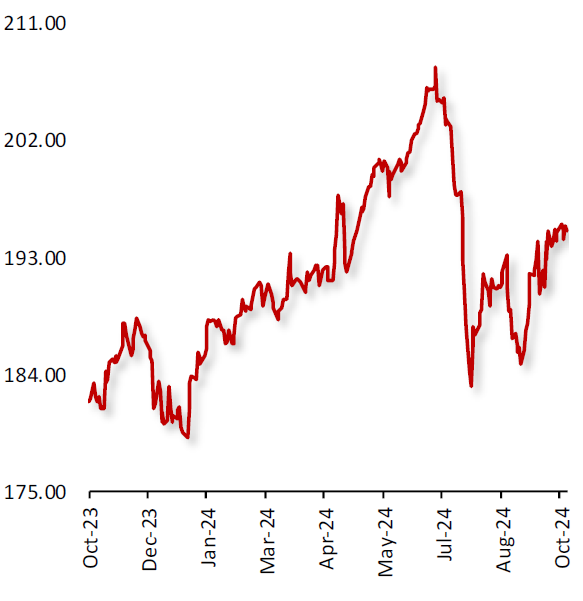

US Oil Fund ($)

|

|

|

Oil Prices Decline Amid Worries Over Global Demand Outlook

|

|

| |

|

|

Oil prices declined this week, amid worries over global demand outlook and as fears over major supply disruption subsided after reports indicated that Israel would not attack key oil facilities in Iran. Adding to the negative sentiment, Chinese authorities failed to provide details on a stimulus plan sufficient to boost investors morale about crude demand.

Also, the Organization of the Petroleum Exporting Countries, further trimmed its outlook for growth in oil demand for 2024 and in 2025, marking the producer group's third consecutive downward revision. China, the world's largest crude oil importer, accounted for the bulk of the 2024 downgrade. Data indicated that, China's crude imports for the first nine months of the year fell nearly 3% from last year to 10.99 million bpd. Meanwhile, global oil output remained strong and is expected to grow.

|

|

| |

| |

| |

|

|

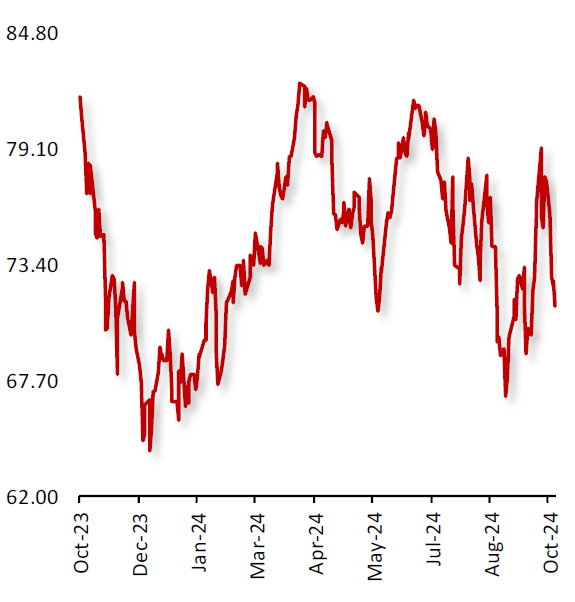

XAU Gold (XAU/USD)

|

|

|

Gold Prices Rise Amid Drop in the US Treasury Yields

|

|

| |

|

|

Gold prices advanced last week, as uncertainty surrounding the US Presidential elections and escalating geopolitical tensions in the Middle East prompted boosted demand for the safe haven asset. Moreover, a series of upbeat US economic data reinforcing expectations that the US central bank will continue its rate-cutting path for the rest of the year.

Additionally, the Benchmark 10-year note yields dropped, following disappointing manufacturing activity data in the New York State.

The central banks remain keen buyers of gold to diversify their reserves for financial or strategic reasons. Global central banks increased purchases for their reserves by 6% to 183 tons in the second quarter, according to the World Gold Council, and are on track to slow buying in full 2024 by 150 tons from 2023. Meanwhile, China's central bank held back on buying gold for a fifth straight month in September.

|

|

| |

| |

| |

|

|

BTC/USD

|

|

|

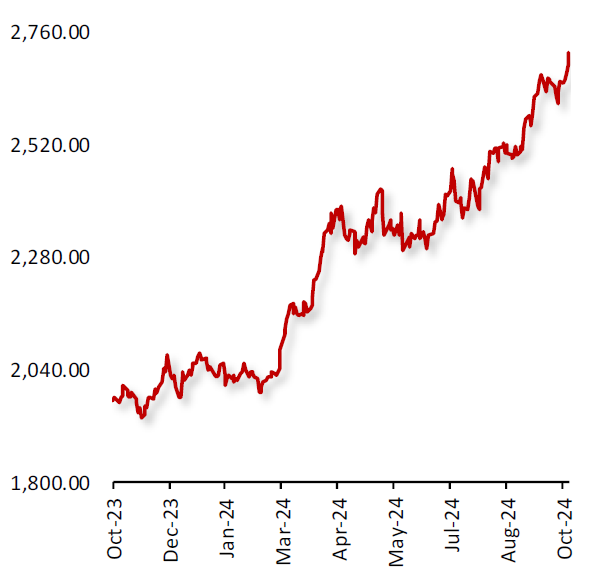

Bitcoin Climbs Amid Hopes Surrounding Bipartisan US Government Support

|

|

| |

|

|

Bitcoin’s price climbed last week, as upward momentum was bolstered by positive global signals and amid optimism surrounding regulatory outlook in the US after November’s Presidential election.

US Vice President Kamala Harris has pledged to support regulatory framework for cryptocurrency and other digital assets. The Democratic Party has not been seen as pro-crypto in the past, and therefore this change in stance has energised the crypto markets. On the other hand, US Republican, Donald Trump has already had a favourable stance towards the crypto industry.

Additionally, interest rate cuts by the major global central banks further supported Bitcoin price. Also, the uncertainty surrounding the scale of China’s economic stimulus measure has prompted capital rotation into alternative assets like BTC. On the outlook front, Bitcoin prices expected to rise further, amid escalating geopolitical tensions in the Middle East.

|

|

| |

| |

| |

|

| |

|

|

|

Key Global Currencies and Commodities

|

|

| |

| |

| |

|

Currency

|

| |

|

| |

|

Commodities & Crypto

|

| |

|

| |

|

|